Cornwall Insight has cut its 2024 power market price forecast for Britain by 12% to an average of £113/MWh.

Included with the market researcher’s fourth 2023 GB Benchmark Power Curve, Cornwall Insight attributed the decline to several key drivers, including the reduced presence of higher marginal cost fuelled technologies (such as gas) in favour of new renewable assets.

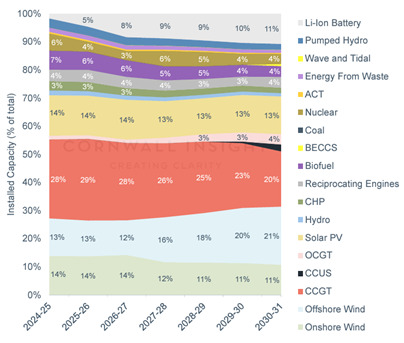

The low marginal cost of solar, onshore and offshore wind, means that prices tended to fall when these assets were generating.

This contributed to the £16/MWh drop in power prices from Cornwall Insight’s previous quarterly forecast; a decline continued until 2026.

Cornwall Insight also noted that the UK’s Emission Trading Scheme (ETS) prices – which implements a price to grant businesses permission to pollute – were also higher compared to the organisation’s Q3 report in October, as demand for allowances have risen.

Despite this increase however, the UK ETS still remains below the EU ETS.

Last Autumn there was some concern over the UK’s falling ETS price. These fears fell into two categories: the UK making polluting cheaper, thus removing incentives for businesses to decarbonise; and the introduction of the EU Carbon Border Adjustment Mechanism (CBAM), that will impose a carbon tax on businesses for imported goods that paid lower tax levels than the EU ETS.

According to Energy UK, if UK and EU ETS price disparities continue, over £500 million per year could be paid by the UK in EU carbon taxes.

Levelling prices above pre-pandemic levels

Despite the decrease in power prices, which Evelin Blom, modeller at Cornwall Insight said would bring “much-needed good news for GB households and businesses,” the forecasts still remain above pre-pandemic levels.

The current £113/MWh average forecast for 2024 is more than double historic averages of £50/MWh, which Cornwall Insight largely attributed to Europe’s dependence on international Liquified Natural Gas (LNG), which saw prices sky-rocket following sanctions on imports from Russia.

Delays to the deployment of offshore wind has also helped maintain higher power prices, continued Cornwall Insight.

Auction Round 5 (AR5) of the Contracts for Difference (CfD) scheme in 2023 saw a major loss for future UK offshore wind capacity as low strike prices deterred any projects from bidding, resulting in no offshore wind projects securing contracts.

The UK government responded to this disappointing outcome, however, and has since increased the strike price for all technologies under the CfD scheme including increasing offshore wind’s strike price by 66%.

According to Cornwall Insight however, the results of AR5 will mean that the UK’s 50GW offshore wind capacity by 2030 target will not be met.

Demand growth caused by electrification towards 2030 will also level power prices above pre-pandemic levels, continued Cornwall Insight, balancing benefits from the deployment of renewables.

Cornwall Insight also noted that increased power exports to Europe will act as a barrier to decreasing power prices in Britain.

Earlier this week (8 January), the second reading of the Offshore Petroleum Licensing Bill took place, which proposes the introduction of new North Sea gas licenses, from which 80% of the energy produced would be exported.

These factors will see the power prices level out to £83/MWh by 2029, according to Cornwall Insight’s forecast – over £40/MWh higher than historic levels.

With lower power prices “on the horizon” Blom expressed her optimism that this trend will “trickle down to consumer bills,” although added the Britain’s consumers still “face a long road to truly affordable energy.”

“Achieving a clean and affordable energy future requires a balanced approach, one that embraces diverse technologies like offshore wind and nuclear alongside smart renewables investment incentives,” added Blom.

“By prioritising affordability, security, and sustainability, we can ensure a brighter energy future for all.”